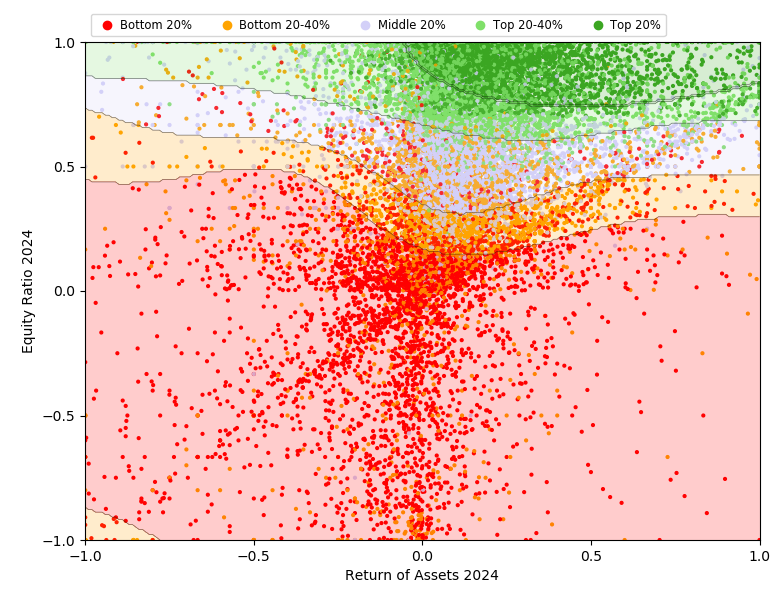

The chart below illustrates how Danish companies are positioned in Valuatum’s rating model based on key financial indicators. In the chart, each point represents one company:

- The horizontal axis shows profitability (return on assets).

- The vertical axis shows solvency (equity ratio).

Companies located in the upper-right corner are typically both profitable and financially solid, while those in the lower-left corner tend to have weaker profitability and solvency. The color of each point indicates the company’s credit rating: green companies represent lower risk, while red companies represent higher risk.

The background color areas indicate which rating is most typical for companies with those particular financial metrics.

If a company’s situation is otherwise typical (meaning there are no exceptional risk factors), the chart provides a good indicative view of the rating level a company would usually fall into.

If the example company’s figures are otherwise neutral, achieving an “A”-level rating (placing it among the top 20% of Danish companies) typically requires an equity ratio of 75–100% and a positive return on equity.

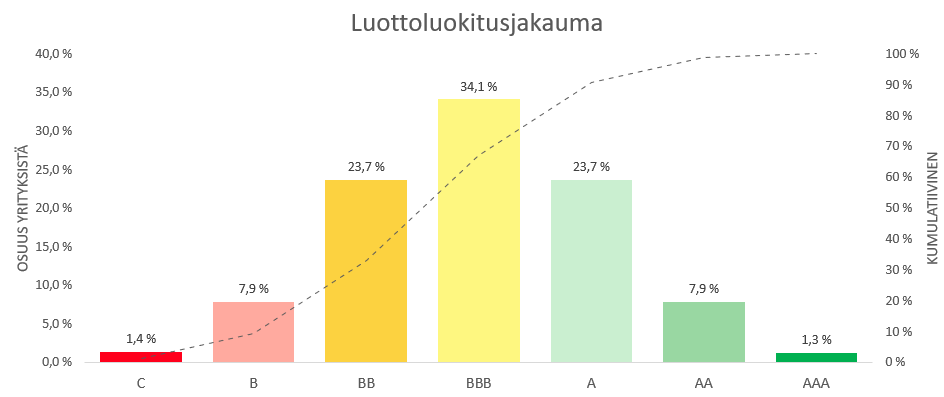

In Valuatum’s model, ratings are calibrated so that only about one third of companies fall into the A categories (see the distribution below). This is broadly consistent with the distributions used by international credit rating agencies such as Standard & Poor’s.

By contrast, some competing services in Finland for example, classify around 90% of Finnish companies into A categories.

In practice, this means that the same company may receive different ratings across different services. Valuatum’s rating may appear lower even though the company’s relative risk level is the same.

The difference does not necessarily reflect a different assessment of the company’s risk, but rather how ratings are distributed across the overall population of companies.

Valuatum’s credit rating distribution

Source: Valuatum

S&P’s credit rating distributionSource: Business Insider

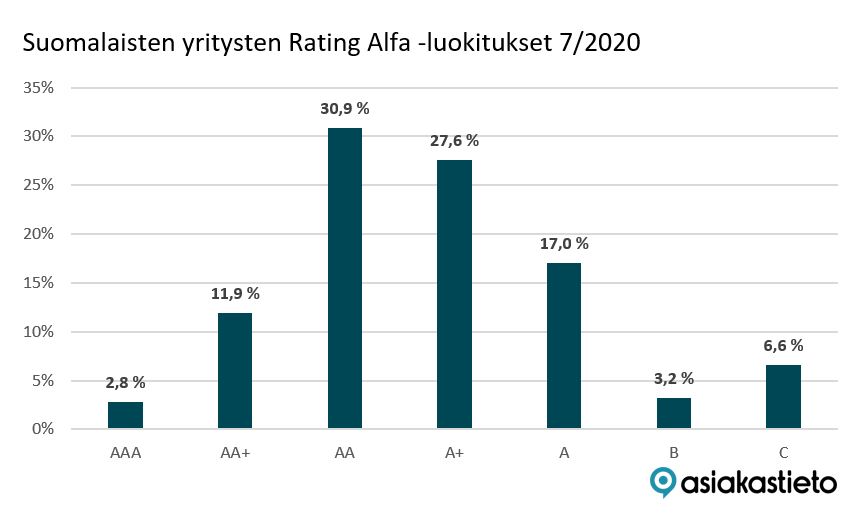

Asiakastieto’s credit rating distribution (owner of Proff.dk)

Source: Kauppalehti

Yes. Different providers use different models, weightings, and data sources, so the same company may receive different ratings across different services.

These differences do not necessarily mean that one assessment is “wrong.” Rather, they reflect different approaches to evaluating risk. A credit rating is always a model-based estimate of how a company compares with other companies and with observed historical risk patterns.